Home > Insights & news > The Allens handbook on takeovers in Australia > Takeover bids (for companies and trusts)

Takeover bids (for companies and trusts)

- A takeover bid can be used for either a friendly or hostile acquisition of a company or trust.

- A takeover bid involves the making of individual offers to purchase target securities at a specified bid price.

- There are two types of takeover bid: an off market bid and a market bid.

- Virtually all takeover bids are off-market bids because of the ability to include conditions.

- Takeover bids are subject to the following key rules that:

- all offers must be the same;

- the bid price cannot be lower than the price which the bidder paid for a target security within the previous 4 months;

- the offer period to be no less than 1 month and no more than 12 months;

- there are no special deals for individual target securityholders;

- there are no self-triggering bid conditions (for off-market bids);

- the bidder must issue a ‘bidder’s statement’ containing the offer terms and other information;

- the target must issue a ‘target’s statement’ containing the target board’s recommendation; and

- the bidder is entitled to compulsory acquisition if it obtains a relevant interest in at least 90% of the target securities (and has acquired at least 75% of the securities it offered to acquire).

7.1 What is a takeover bid?

In general terms, a takeover bid involves a bidder making individual purchase offers at a specified bid price to all holders of securities in an ASX-listed Australian company or trust. If, by the end of the offer period, the bidder has received acceptances of the offers sufficient to give it a relevant interest in at least 90% of the target securities (and has also acquired at least 75% of the securities it offered to acquire), the bidder can proceed to compulsorily acquire the remaining target securities at the bid price.

There are two types of takeover bid:

- an off market bid (which may offer cash or other consideration, may be subject to conditions, and may be for 100% of the target securities or a specified proportion of each target securityholder’s securities); and

- a market bid (which must be an unconditional cash offer).

In an off-market bid, the bidder must make its offers to target securityholders in writing in a document called a bidder’s statement. The target must respond to that by preparing and despatching to its securityholders a document called a target’s statement which contains the target directors’ recommendation. In contrast, a market bid (often called an on-market bid) involves the bidder appointing a broker to stand in the ASX market and make offers to acquire target securities at the specified bid price, with acceptances being effected by the execution of on-market trades rather than off-market acceptances. Despite the offers being made on-market, a bidder’s statement and target’s statement still needs to be prepared in a market bid.

A takeover bid, whether an off-market or market bid, can be used for either a friendly or hostile acquisition. In a friendly deal, it is common for the bidder and target to enter into a bid implementation agreement which contains: the agreed key terms and conditions of the offer, the target’s obligations to recommend the bid, and various other provisions dealing with the operation of the target prior to the bidder obtaining control of the target. It is also common for a bid implementation agreement to contain deal protection mechanisms such as exclusivity provisions (including ‘no-shop’ and ‘no-talk’ restrictions), rights to match rival bidders and a break fee payable by the target to the bidder in certain circumstances if the bid is not successful. A bid implementation agreement is binding only on the target and not on target shareholders.

Virtually all takeover bids are off-market bids because of the ability to include conditions. For simplicity this handbook focuses on the off market bid structure involving an offer for 100% of a target’s securities. This section 7 focuses on the key takeover rules and features. See sections 10 and 11 for a discussion of the strategic considerations involved in planning or responding to a takeover proposal.

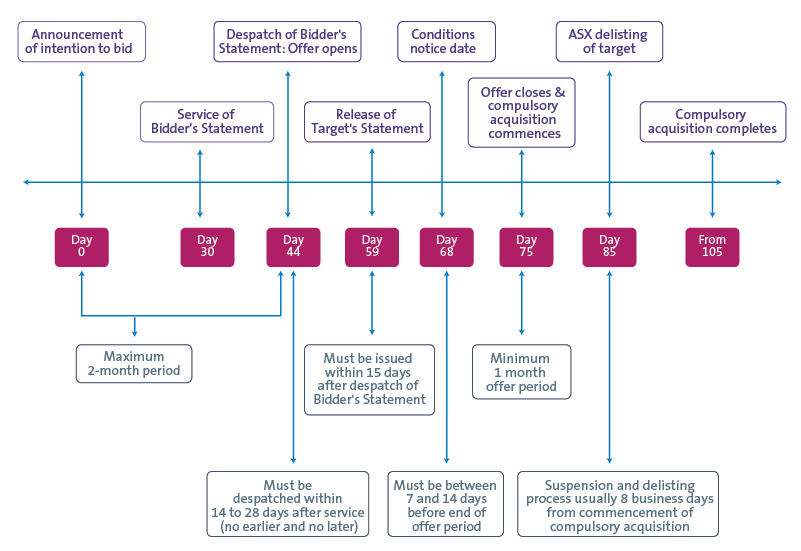

7.2 Indicative timetable

Below is an indicative timetable for a basic off-market takeover bid, which assumes that the bid becomes unconditional, does not require any extensions and proceeds to compulsory acquisition. It is also assumed that there is no rival bidder and no regulatory action which affects timing.

7.3 Key takeover bid rules and features

The rules governing an off-market takeover bid are detailed in Chapter 6 of the Corporations Act, and supplemented by ASIC and Takeover Panel policies. Below is a summary of the key takeover bid rules and features.

(a) Bid announcement and 2-month rule

It is standard practice for a bidder to first announce an intention to make a takeover bid for a target before lodging and despatching its bidder’s statement. The making of a bid announcement triggers an obligation on the bidder to despatch its bidder’s statements (which contain the takeover offers) within 2 months. This is commonly known as the ‘2-month rule’. The terms and conditions of the takeover offers must be the same or not substantially less favourable (to target securityholders) than those in the announcement. Because of this the proposed offer conditions (see paragraph (h) below) need to be set out in full or described in detail in the announcement.

There are limited circumstances in which a bidder need not follow through. These include where a bidder could not reasonably be expected to proceed with the takeover bid as a result of a change in circumstances, eg an offer condition being breached or the bidder has been clearly overbid.

(b) Offers must be the same

All the offers made under the bid must be the same, subject to certain statutory exceptions.

(c) Offer consideration

There are no restrictions on what can comprise offer consideration. It can be in the form of cash (in any currency), securities (whether quoted or unquoted) or other non-cash assets, or a combination of those, provided that all target securityholders are offered the same thing. A bidder can offer consideration alternatives (eg cash or shares), again provided that all target securityholders are offered the same alternatives.

If the offer consideration comprises cash, the bidder’s statement must contain details of the source of that cash consideration (eg cash at bank, funding from parent entity, external debt financing or equity raising). A bidder should not announce a bid without either adequate funding arrangements already in place or reasonable grounds to expect that it will have sufficient unconditional funding in place to satisfy acceptances when its offers become unconditional. Reasonable grounds may still exist even if any debt financing has not been formally documented or remains subject to conditions to drawdown at the time of announcement, but there must be an enforceable commitment.

If the offer consideration comprises securities, the bidder’s statement must contain prospectus-level disclosure regarding the assets, liabilities, profits and prospects of the issuing entity and particulars of the securities being offered.

The offer consideration can be increased, but not reduced, during the course of a bid. All target securityholders who have already accepted the bid are entitled to receive any increase. If the bidder acquires target securities on-market or otherwise outside the takeover bid during the offer period at a price higher than the bid price, the offer is deemed to be increased to that price. If the original offer did not include a cash-only consideration and the bidder purchases target securities outside the bid for cash, the bidder must give offerees who have accepted the opportunity to elect to receive cash.

(d) Minimum bid price rule

The consideration offered for target securities must equal or exceed the maximum consideration that the bidder or an associate provided, or agreed to provide, for a target security under any purchase or agreement during the 4 months before the date of the bid. There are particular rules for determining the value of pre-bid non-cash consideration, and for applying this rule where the consideration under the bid is or includes scrip.

(e) Time limits for payment of consideration

In general terms, the offer consideration must be paid or provided by the earlier of 1 month after the offer is accepted (or if the offer is subject to a defeating condition, within 1 month after the contract becomes unconditional) and 21 days after the end of the offer period. It is common for bidders to accelerate payment timeframes to attract acceptances, once the offer is unconditional.

(f) Length of offer period

The offers must remain open for at least one month. The offer period can be extended by a further period, subject to an aggregate offer period of not more than 12 months. Most bids are made for the minimum period of one month and then extended as necessary to secure sufficient acceptances. If the offer is conditional, any extension must be effected before the ‘status of conditions’ notice is filed (see paragraph (h) below for a description of this notice). The only exception to this is where a rival takeover bid is announced or improved during that last 7-day period. The offer period will be automatically extended if within the last 7 days the consideration is improved or the bidder’s voting power increases to more than 50%. In that case, the offer period is extended by 14 days from the relevant event.

If the offer period is extended by more than 1 month (or by a cumulative period of more than 1 month) while the offer remains conditional, every target securityholder who accepted the offer before the extension is entitled to withdraw their acceptance.

(g) Collateral benefits rule

The bidder cannot give or agree to give a benefit to a person outside the benefits offered to all target securityholders under the bid if it is likely to induce the person to dispose of their securities or accept the offer under the bid. Technically speaking, such benefits (known as collateral benefits) are only prohibited where given or offered during the offer period, however, the Takeovers Panel’s application of the fundamental takeover principle of ‘equality of opportunity’ means that there is a risk of the Panel making a declaration of unacceptable circumstances in relation to a benefit given prior to, or agreed to be given after, the offer period. As a general rule, a benefit is less likely to constitute unacceptable cirmcumstances if it is given on arm’s-length terms (eg the bidder acquiring an asset from a target securityholder for no more than market value), but would still constitute a collateral benefit if given during the offer period and is likely to induce the target securityholder to dispose of their shares or accept the takeover bid.

(h) Conditions to the offers

An off-market bid can be made subject to conditions which, if triggered, will enable the bidder to let its bid lapse and all acceptances will be voided. There are restrictions on what conditions can be imposed. In particular, a condition cannot be ‘self-triggering’, ie. dependent on the bidder’s opinion, events within its control or events which are a direct result of the bidder’s actions. This means that a general due diligence condition is not possible, though it is possible to craft due diligence-type conditions linked to objectively determinable outcomes (eg that the target maintain a specified minimum cash position or publicly confirm that a certain state of affairs exists or does not exist). Also, there cannot be any maximum acceptance condition (one triggered if acceptances exceed a specified level). A bidder can waive conditions of its offers, but must do so at least 7 days before the offers close (the exception to this is what are called prescribed occurrence conditions which are a very narrow category of circumstances in relation to the target – see below).

Common bid conditions include: minimum relevant interest threshold (often 90% to tie in with the compulsory acquisition threshold), regulatory approvals (eg foreign investment approval or anti-trust approval), no material adverse change in relation to the target, no material transactions by the target, and no ‘prescribed occurrences’ in relation to the target (eg no new equity issues, no insolvency events, and no sale of the main undertaking).

The bidder must nominate a date, which must be between 7 and 14 days before the end of the offer period, on which it will notify the market on the status of its bid conditions. This date will usually be extended by the same period as any offer period extension.

(i) Bidder’s statement

The offers despatched to target securityholders must be accompanied by or contained in a bidder’s statement. This document requires a considerable amount of preparation on the part of the bidder and its advisers. It is required to contain all information known to the bidder which is material to a decision by a target securityholder whether or not to accept the offer. It is also required to contain a range of statutory disclosures, including:

- a statement of the bidder’s intentions regarding the continuation of and any major changes to be made to the target’s business, and the future employment of present employees;

- where cash is offered as consideration, the funding sources of that cash; and

- where securities are offered as consideration, information to prospectus disclosure standard regarding the assets, liabilities, profits and prospects of the issuer and particulars of the securities being offered.

The bidder cannot despatch its bidder’s statement and offers to target securityholders earlier than 14 days after service of the bidder’s statement on the target (unless the target directors consent to early despatch, which often occurs in a friendly takeover bid). A bidder’s statement must be despatched no later than 28 days after service on the target, and within 2 months after the bidder has announced its intention to make a takeover bid.

In a hostile bid situation, the target board will normally use the 14-day waiting period to review the bidder’s statement to determine whether there are any aspects which require clarification for securityholders. If the bidder’s statement is considered to be defective in any way, or appears to contain material misstatements or omissions, the target board can make an application to the Takeovers Panel for a declaration of unacceptable circumstances and orders for corrective disclosure. In practical terms, any such application should be brought no later than the end of the first 7 days of that 14-day period.

(j) Target’s statement

After receipt of the bidder’s statement, the target must prepare and despatch to its securityholders a target’s statement responding to the bid. The target’s statement must contain a statement by each target director recommending that the bid be accepted, or not accepted, and giving reasons for the recommendations, or reasons why a recommendation has not been made. It must include all information known to any target director that target securityholders and their professional advisers would reasonably require to make an informed assessment whether to accept the bid.

Once the 14-day waiting period expires and the bidder despatches the bidder’s statement to target securityholders, the target then only has 15 days to finalise preparation of its target’s statement and print and commence despatch of that target’s statement to its securityholders. This can place considerable pressure on a target which is subject to a hostile bid.

If the bidder’s voting power in the target is 30% or more, or a director of the bidder is also a director of the target, then the target’s statement must be accompanied by an independent expert’s report. That report must state whether, in the expert’s opinion, the offer is fair and reasonable. It is also possible that the target will wish to obtain an independent expert’s report as part of its defence, which would accompany the target’s statement. The independent expert’s report will be a long-form report, giving a detailed assessment of the value of the target and its securities, as well as a (usually less detailed) assessment of the value of the bidder’s offer consideration, if for example it includes scrip.

(k) Getting to 90% – the ‘chicken and egg’

A key issue for a bidder looking to acquire 100% under a takeover bid is that, while the bid will be subject to a 90% minimum acceptance condition, institutional investors often will not accept while the bid remains conditional. This means that bidders will generally need to waive the offer conditions in order to reach the 90% compulsory acquisition threshold – though this exposes the bidder to the risk of ending up with less than 90% or even with a minority interest. It is largely because of this risk that the scheme structure, which provides an ‘all-or-nothing’ outcome, is frequently used to effect a ‘friendly’ 100% acquisition of a target.

One tool which has been developed to attempt to deal with this issue in a takeover bid is the institutional acceptance facility, which has been used in numerous takeover bids. The concept is simple. Rather than accepting the bid at the outset, certain institutional target securityholders are given the option of initially just indicating their intention to do so. That is achieved by the institution providing ‘acceptance instructions’ to a third-party trustee. The instructions either take the form of a completed acceptance form or (if the securities are held through a custodian) written directions to the custodian. The trustee holds the instructions until a specified trigger event occurs – most commonly the delivery of a notice by the bidder confirming that, when combined with the actual acceptances already received by the bidder, the instructions will (when processed) result in the bidder achieving acceptances for more than a specified percentage of the target (such as 50% or 90%) and the bid will then become unconditional.

Upon the trigger event occurring, the trustee acts on the instructions by delivering the acceptance forms to the bidder and providing the directions to the custodians. Hence, it is only at that point that the institutional securityholders’ intentions to accept are converted into actual acceptances of the bid. Up until the trigger event occurring, the securityholders have the ability to retract their instructions, and retain full control over the voting and disposal of their securities.

Such facilities have an in-built flexibility which makes them attractive to bidders: they can be introduced at any time during a bid and (within limits) the bidder has a broad discretion as to what trigger event applies. This flexibility is particularly useful. A bidder has the opportunity of first assessing the bid’s progress before having to commit to withdrawal rights. If such rights become necessary, they can then be tailored to the particular circumstances prevailing – the facility can be directed at the specific securityholders that have concerns, and can be structured with a trigger event that achieves the precise outcome desired by the bidder.

(l) Compulsory acquisition

If at the end of the offer period the bidder has received acceptances sufficient to give it relevant interests in 90% or more of the target’s voting securities, the bidder can proceed to compulsorily acquire the remainder at the bid price. This process usually takes about 1 to 2 months to complete. In theory the bidder can commence the compulsory acquisition process during the offer period provided the 90% threshold is met, but it is usual to wait until the offer period has ended.

(m) Liability regime

The Corporations Act contains a detailed liability regime for misleading or deceptive statements or conducts in relation to takeover transactions.

There is a specific regime covering bidder’s statements and target’s statements. Broadly, the inclusion of a misleading or deceptive statement in such a document, or an omission of required information from such a document, is prohibited and gives rise to a requirement to compensate any person who suffered loss as a result, and can also give rise to criminal liability. Each director of the bidder or target automatically bears liability if the bidder or target (as applicable) has issued a defective bidder’s statement or target’s statement (as applicable).

Defences against criminal and civil liability for a defective bidder’s statement or target’s statement include: that the relevant person proves they did not know the statement was misleading or deceptive or that there was a relevant omission; or the relevant person (if a director) proves that they placed reasonable reliance on the company’s management; or the relevant person (if a company) proves that they placed reasonable reliance on an external adviser. It is common practice for bidders and targets to establish due diligence processes to assist in establishing these defences if required, in addition to minimising the risk of including a misleading or deceptive statement in a bidder’s statement or target’s statement in the first place.

Foreign Investment in Australia

Managing complex foreign investment approvals for those investing into Australia from overseas, expanding existing Australian business through acquisitions, or running a sale process that will attract foreign interest.

Get in touch

Connect

Allens is an independent partnership operating in alliance with Linklaters LLP. © 2020 Allens, Australia